Last Quarter Performance

The Aussie was very much in an uptrend through Q2 as it pushed up from the annual low (0.5915) early in April to then hit an annual high (0.6590) towards the end of the quarter. There were some choppy moves along the way, however, the Aussie maintained smooth trading conditions for the majority of the quarter as it ground its way higher.

Domestic Data

Australian data has certainly pulled back further over the last few months, with both key inflation and employment numbers all dropping lower. The May CPI data came in lower than expected, dropping to 2.1% from 2.4% which was a substantial decrease and had the market anticipating a cut from the RBA in July, and jobs numbers had also disappointed the week before with the first negative print in over a year.

Reserve Bank of Australia Expectations

The Reserve Bank failed to deliver a well-anticipated rate cut in July, which sent a shock wave through Australian markets that had been pricing in a 95% chance of a 25-basis point easing. The board, which had been resolutely hawkish up until the May meeting, is clearly still concerned with inflation, and the June quarter CPI update looks to be key for continued easing from the central bank.

The good news for doves is that Governor Michelle Bullock has advised that the bank anticipates cuts coming in H2, and this could add some pressure to the currency, especially if we see a change in sentiment for the greenback. Upcoming data will be key to the RBA’s thinking, and traders are expecting to see some strong moves if we see significant deviations from expectations.

Commodity Influence

Iron Ore has just completed its best run since January, and this has also helped support the currency, whilst Gold is also sitting close to all-time highs. There is no doubt that currency traders will be keeping a close eye on the impact of US tariffs on commodity prices and demand in the coming weeks and months, as they will have a significant impact on the Aussie dollar. The government’s latest report has lowered its revenue forecast for the Australian commodity industry on the back of global trade concerns, and this could weigh on the currency over time.

Traders will continue to monitor pricing and demand across Australia’s major commodity exports, with any significant moves likely to weigh on the currency.

Geopolitical Influences

There is no doubt that US tariffs and President Trump’s trade plans have been one of the biggest influences on currency moves in the year so far, and that looks set to continue.

The market has resolutely shrugged off most of the concerns that were evident on the initial announcement, and we have seen the greenback pull back to multi-year lows as a consequence, which has helped the Aussie and the other majors to rally strongly.

Tariff updates and the impact of implementation that is now scheduled for August will have a big effect on data over the coming months, and we may see even more volatility as we progress through the quarter.

China’s progress will, as always, be closely monitored by Aussie traders with signs of a resilient economy in the face of global trade concerns likely to lend support to the currency and any signs of further slowing likely to lead to downside corrections.

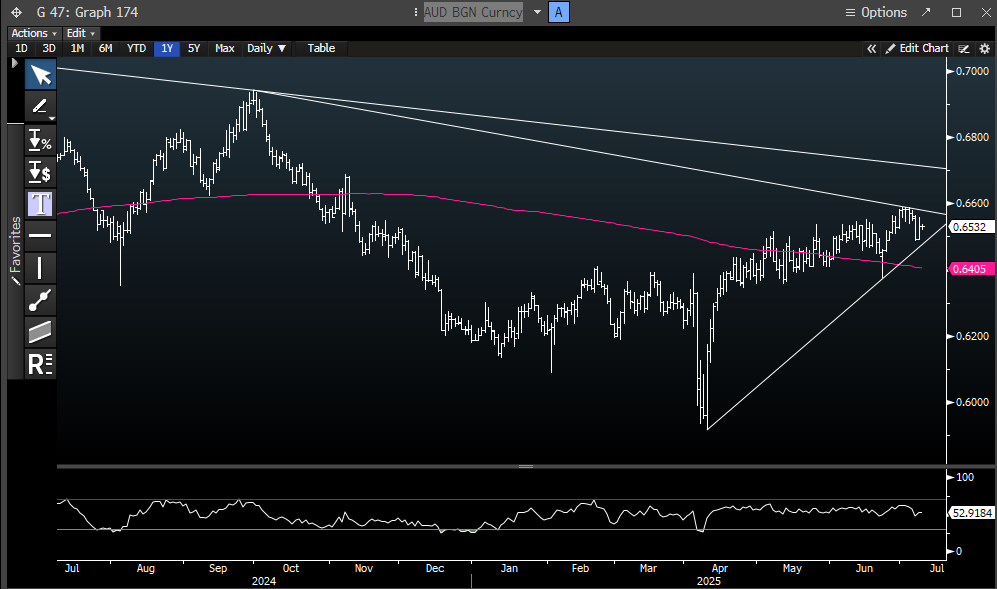

Technical Analysis

A continued depreciation in the US dollar could see the Aussie break higher into fresh topside ranges as we progress into Q3, with the long-term trendline resistance on the daily chart coming in around 0.6700. A change in the big dollar momentum, which would likely come from a hard tariff implementation, could see some sharp corrections for the Aussie and push it back into last quarter’s ranges with initial support now sitting on the daily trendline support around 0.6500.

Resistance 2: 0.6703 – Long-term Trendline Resistance

Resistance 1: 0.6595- Short-term Trendline Resistance and 2025 High

Support 1: 0.6501 – Trendline Support

Support 2: 0.6373 – June Low