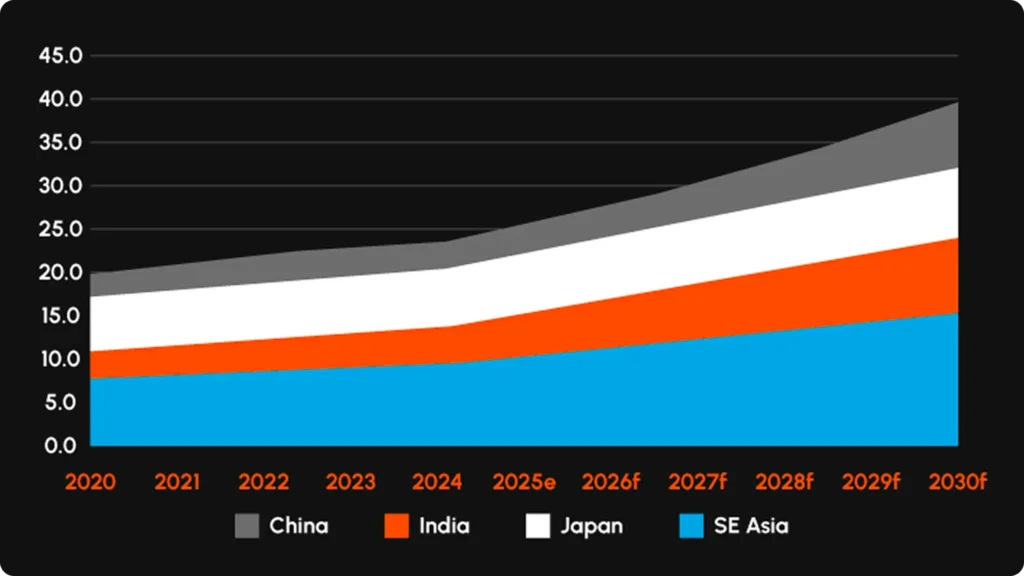

Asia is poised for a revolution in asset under management that will significantly boost the global fund management industry. By 2030, assets under management (AUM) in the region are projected to reach an impressive $45 trillion, representing nearly 30% of the global total. This substantial growth, lifting Asia’s current share from 18–20% — or $23 trillion — to just under 30% ($27 trillion), signals a structural shift in the management of the world’s capital.

But it is also clear that global assets under management is skyrocketing, rising from $115 trillion to $165 trillion, or $50 trillion —an increase of 43% from the 2020 level. That means it’s not just Asia that’s seeing a sharp rise in assets under management, but that we are witnessing a global phenomenon.

Chart 1: Growth in Asian asset markets

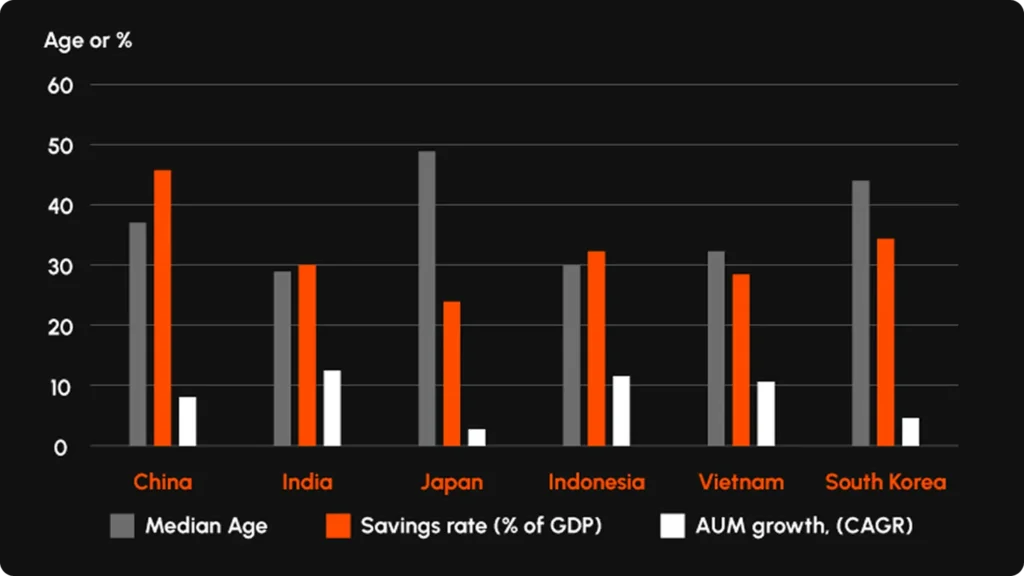

Demographics and Savings go Hand in Hand

Demographics stand as the most potent catalyst behind Asia’s ascent. India, Vietnam, and Indonesia boast some of the youngest populations globally, with median ages under 33. This youth bulge is entering the workforce, earning, saving, and investing at unprecedented rates, shaping a unique narrative of growth and potential in the region

India is a striking example. Over the past decade, the number of mutual fund investors has surged from fewer than 20 million to more than 150 million. Systematic Investment Plans (SIPs), where retail investors commit small monthly sums, have become a cultural phenomenon. In 2024 alone, SIP inflows exceeded $20 billion, demonstrating how a youthful, digitally savvy population is reshaping the investment landscape.

China, by contrast, is ageing rapidly, with a median age approaching 40. Yet its high savings culture — with household savings rates above 40% of GDP and a population of 1.4bn — continues to underpin its dominance. Even as economic growth slows, the sheer scale of Chinese savings ensures that its fund management industry remains the largest in Asia.

Japan and South Korea, though older, provide institutional depth and leadership in ESG integration. Their pension funds and insurance companies are among the largest in the world.

Chart 2: Strong link between savings and ageing:

The Role of Technology

Asia’s fund management boom is intricately intertwined with its digital revolution. The rise of mobile-first platforms is democratising access to investment products, particularly in India and Southeast Asia, ushering in a new era of accessibility and inclusivity. In markets with thin traditional financial infrastructure, smartphones have become the gateway to investing, reshaping the financial landscape in Asia.

Retail investors, once on the sidelines, now contribute over 40% of AUM growth in the region, a significant increase from 25% a decade ago. Investing is no longer the exclusive domain of the wealthy; it is becoming a mass market activity, reshaping the financial landscape in Asia.

Digital adoption is also reshaping fund structures. Blockchain based settlement, AI driven portfolio management, and robo advisory services are no longer fringe experiments. They are the driving forces behind the reshaping of fund structures in Asia, showcasing the transformative power of technology across the industry.

ESG and the Asian Model

Environmental, social, and governance (ESG) investing is often seen as a Western construct, but Asia is rapidly developing its own brand of ESG investing. Japan and South Korea are at the forefront, embedding ESG principles into pension funds and institutional mandates.

China, meanwhile, is scaling green finance at speed. It is now the world’s largest issuer of green bonds, with cumulative issuance exceeding $300 billion. The government’s commitment to peak carbon emissions before 2030 and achieve carbon neutrality by 2060 has created a powerful policy tailwind. Asset managers are responding by launching green funds, ESG indices, and climate focused investment vehicles. It also has global-leading capabilities in the manufacturing of wind farms and solar panels.

Global Implications

Asia’s savings increase has implications for global investors and policymakers. Here are some main reasons why:

• Capital Flows: With nearly one in every three dollars of the world’s managed assets based in Asia, global capital allocation will increasingly be influenced by Asian.

• Regulation: Asian regulators, from the Monetary Authority of Singapore to China’s CSRC, will play a larger role in setting international standards.

• Competition: Western asset managers will need to localise products, embrace digital platforms, and adapt to Asia’s retail driven growth if they are to remain competitive.

Table 1: Global savings to rise

Risks and Challenges

The path to $45 trillion is unlikely to be smooth. Geopolitical tensions, regulatory fragmentation, and uneven capital market development could slow progress. Demographic ageing in China, Japan, and South Korea will also weigh on long term growth.

Yet the structural drivers — demographics, savings, and technology — remain robust enough to sustain Asia’s trajectory. Even amid short term volatility, the long term trend is clear: Asia’s share of global AUM is rising rapidly.

Conclusion: A More Equal Pillar of Global Financial Markets

By 2030, Asia will be a very influential force in global fund management. It will be an equal participant, joining the US and Europe in shaping the rules and flows, and will be a key contributor to the industry’s future. For investors, policymakers, and asset managers worldwide, it will be evident that the centre of global gravity in fund management is shifting. That means the time for ‘early mover’ advantage, in brand recognition, organisational structure, and asset positioning, is now.