The Federal Reserve’s July 2025 decision to hold interest rates at 4.25%-4.50% reflects a complex policy posture: growth is rebounding, inflation remains elevated, and political scrutiny is intensifying. Despite a robust 3.0% annualised pace of GDP expansion in Q2, the Fed’s cautious stance is evident in the underlying indicators – sluggish domestic demand, softening labour markets, and persistent inflation. The Fed’s communication strategy, which underscores its unwavering commitment to a data-dependent approach, is navigating dual dissent from Governors Bowman and Waller, and political pressure from the Trump administration, which may have prompted one of the latter to say they will resign in the coming months. That will open the door for the President to appoint one of his supporters to the Fed, making it more malleable to his pressure in future.

This article evaluates a wide spectrum of indicators – production, GDP, price inflation and labour market trends – to explain the Fed’s decision to hold rates and assesses its credibility in the face of political pressure to cut interest rates.

Robust headline growth mask underlying weakness

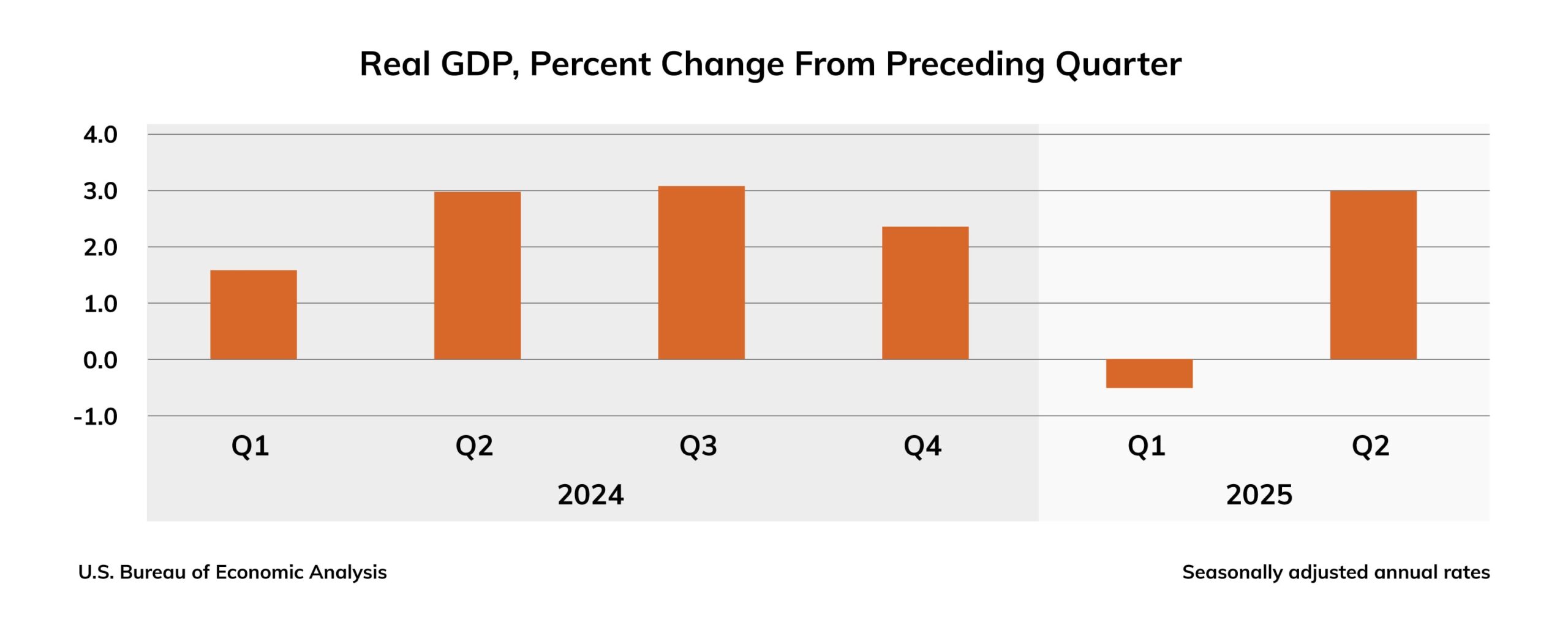

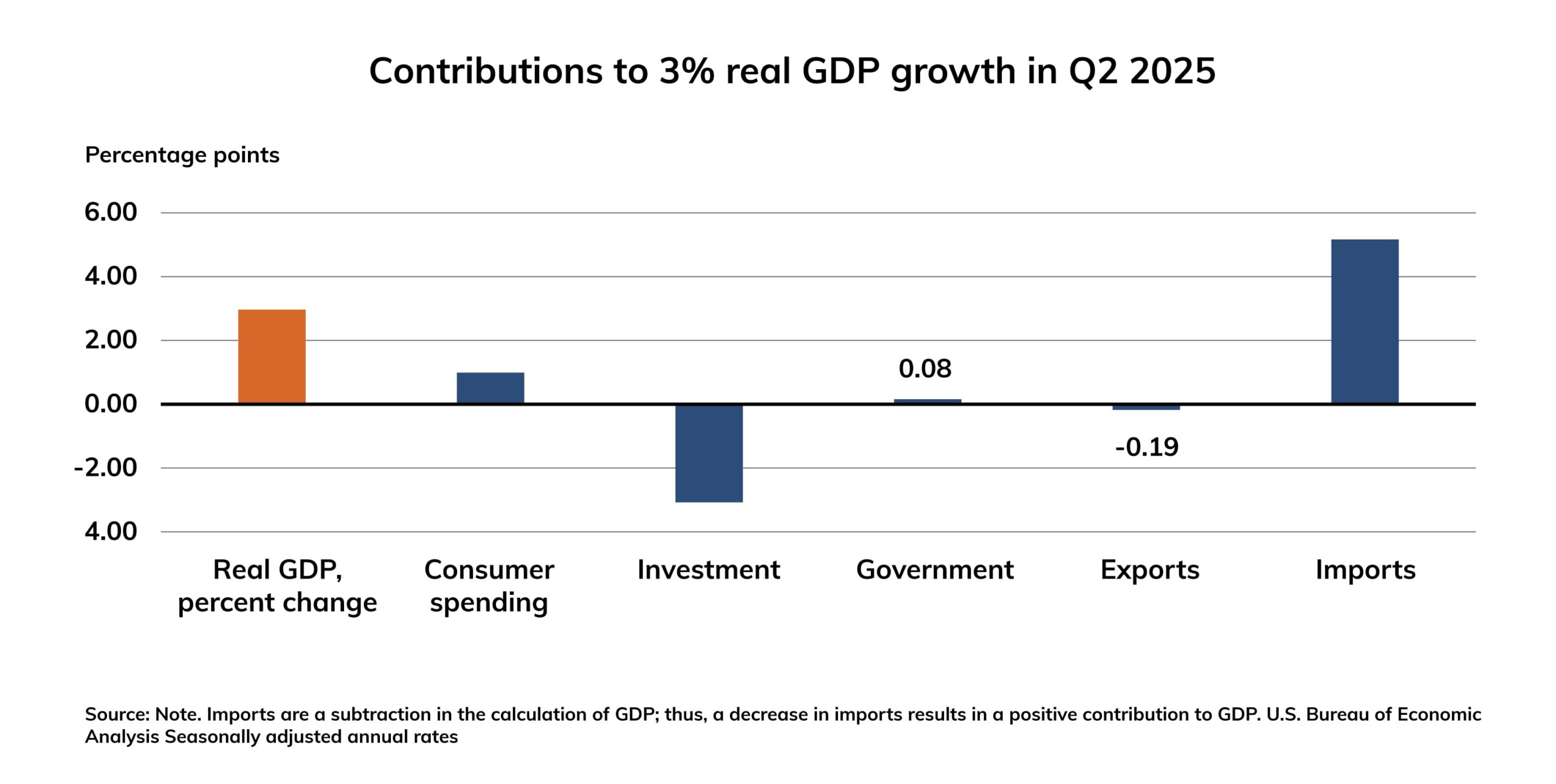

Real GDP rebounded strongly in Q2, registering a 3.0% annualised gain that reversed the 0.5% contraction seen in Q1, see chart 1. Yet much of this strength stemmed from a sharp swing in trade flows: net exports contributed an unprecedented 5.0 percentage points to growth, while inventory drawdowns subtracted 3.17 points-signaling firms were running down stockpiles rather than ramping up new activity. Final domestic demand, which strips out trade and inventories, grew just 1.2% on the quarter, down from 1.9% in Q1, see chart 2.

Chart 1: Annualised US GDP growth jumped in Q2

Chart 2: Imports rise ahead of tariffs and investment falls

Source: Note. Imports are a subtraction in the calculation of GDP; thus, a decrease in imports results in a positive contribution to GDP. U.S. Bureau of Economic Analysis Seasonally adjusted annual rates

Meanwhile, inflation data soften

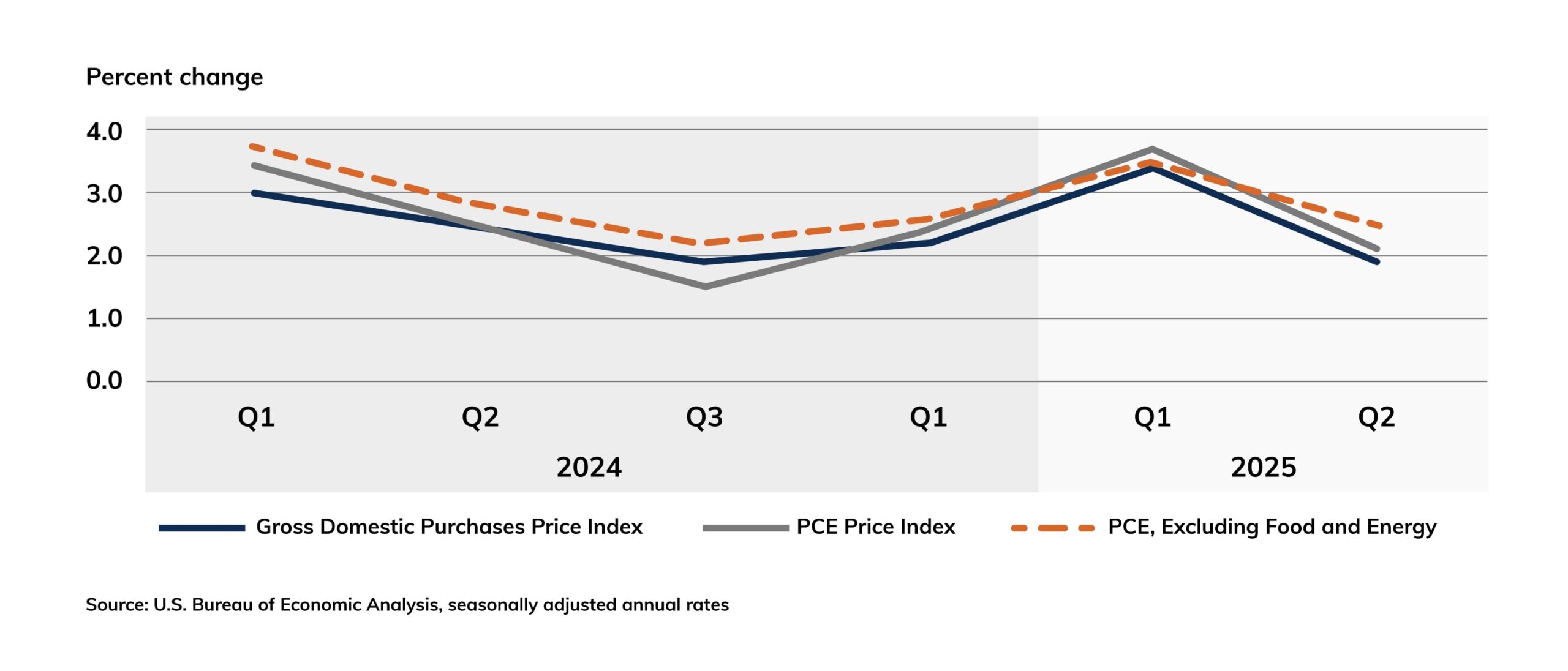

Inflation metrics continue to edge toward the Fed’s 2% goal but remain elevated and vulnerable to trade and related shocks. The PCE price index rose 2.1% year-on-year in Q2, down from a 3.7% advance in Q1, while core PCE (excluding food and energy) slowed to 2.5% from 3.5%. The Consumer Price Index for urban consumers climbed 0.3% in June and stood 2.7% above a year ago, driven in part by shelter and housing costs and tariff-inflated durable goods prices, see chart 3. The latter trend indicates that, with fresh rounds of tariffs set to take effect, their impact is not yet fully reflected in the data, and therefore there’s ample upward price pressure from this source. It is therefore no surprise that the Fed warned of upside risks to inflation, though there is some asymmetry from tariff risks, as slower growth implies lower price inflation pressure.

Chart 3: Price inflation may be falling but upside risk is elevated by tariffs

Source: U.S. Bureau of Economic Analysis, seasonally adjusted annual rates

Labour markets data are mixed

After months of torrid hiring, the U.S. jobs engine is beginning to sputter. Payrolls increased by just 73,000 in July, well below consensus, as the unemployment rate ticked up to 4.2%. Revisions to May and June data peeled back earlier gains by over 250,000 jobs, suggesting underlying demand is cooling and that the impact of tariffs is beginning to wind its way through to hiring. Business surveys reinforce this picture: the ISM services index fell to 50.1 in July from 50.8, and its employment component slipped to 46.4, consistent with further softening in non-farm payrolls heading into the second half of 2025. Remember that the tariffs have not yet come into force, but the uncertainty already appears to be having some impact. This could portend terrible news if the tariff levels, which on average look like they’re going to be around 20 to 30 times the previous average, paint a very negative picture.

Paradoxically, unless this is accompanied by inflation, it could make an easing of rates more likely rather than less likely. But then again, the picture on that score is mixed because if tariff levels are as high as seems likely, then it means that fewer firms are going to be able to resist the pressure to pass through these price rises to final consumers, which will push up CPI and other inflation metrics.

Political pressure mounts…

The Fed’s independence has been tested in recent months by public appeals from President Trump to cut rates – a request Powell declined to heed. Yet two Governors, Michelle Bowman and Christopher Waller, dissented in favour of a 25 bp cut, marking the first dual dissent since 1993. One has since announced an intention to resign. Their stance, which could potentially impact the Fed’s credibility, highlights the tension between data-driven policy and partisan pressure, raising questions about the Fed’s institutional cohesion and credibility.

…but financial markets are relieved by his response

Financial markets greeted the hold decision with muted relief that the Fed stood up to political pressure. Treasury yields drifted higher on renewed uncertainty over the timing of rate cuts, and the dollar strengthened against major currencies. Looking ahead, the Fed emphasised that policy remains “data-dependent,” underscoring its willingness to pivot if growth cools further or inflation proves sticky but not to bow to political pressure. Yet with GDP growth outpacing expectations, inflation still above target, and labour markets loosening only gradually (though recent revisions showed more weakness than hitherto), any near-term easing appears off the table. Still, the September odds of a Fed cut have risen, which is to be expected based on recent trends in the balance of recent data.

Navigating the Political-Economic Nexus

The Fed’s rate hold wasn’t just a monetary decision – it was a testament to the institution’s commitment to stability. Despite strong headline growth and cooling inflation, policymakers chose restraint due to underlying economic fragility and asymmetric risks tied to tariffs and fiscal uncertainty.

Chair Powell’s emphasis on data-dependence sought to reinforce credibility, but dissent and external pressure have revived concerns about central bank autonomy. As Q3 unfolds, the Fed faces a narrowing path: react nimbly to evolving data while maintaining market and institutional trust.

How it navigates this terrain may redefine its role in a politically volatile landscape. It will also determine to what extent global financial markets continue to trust that the Fed’s actions are based on fact and not political pressure. That is crucial since the US underpins the world’s financial payments system with the deep liquidity that is available to lenders and borrowers, and the open markets it supports. That is underpinned by trust in the US Federal Reserve’s governance structure and that it acts objectively rather than is driven by political factors.

The Fed’s July decision underscores its unwavering commitment to preserving credibility in an increasingly politicised environment. While economic data provided legitimate grounds for caution, moderating inflation, trade volatility, and Labour market fatigue, the optics of political dissent and public pressure challenge the perception of central bank independence.

Looking ahead, financial markets’ attention will focus on three critical issues:

- Inflation stickiness: particularly in tariffs-sensitive categories.

- Labour market resilience: can consumer demand be sustained amid wage growth deceleration?

- Fiscal spillovers: how will looming budget cliffs and policy uncertainty affect growth?

- Leading indicators – what do they suggest about future trends in growth and inflation

The Fed’s future decisions will also be significantly influenced by fiscal trends, which indicate a significant deterioration in the budget deficit and underlying debt. This could potentially heighten financial market risks, especially as the fiscal deficit is set to expand with the implementation of the ‘Big Beautiful Bill’. The financing of the debt by overseas investors will consequently increase, as US domestic savings are insufficient to meet its investment needs.

All of this suggests future risks for US credit markets and the US$ as a reserve currency, as well as the credibility of Fed policy, which could play into worries about global financial market fragility.

Conclusion

However, by standing firm under political pressure, Powell signalled that financial markets should be confident in the procedural integrity of the US Fed, at least under his stewardship. Yet as Q3 unfolds, the Fed may face a narrowing path between maintaining credibility, reacting to data, and managing external expectations – both political and market-driven. Powell’s position as Fed chairman could be at risk if he makes a misstep in that delicate dance, potentially impacting the Fed’s credibility and his role.